Home » Finance

Category Archives: Finance

New “Pension Legacy” Tax Proposed – Urgent Legislative Alert – House Bill 711

Double Taxation – the fallacy of pension legacy costs.

I am writing to alert you to a potential property tax increase coming from the Georgia General Assembly. House Bill 711, sponsored by Rep. Mary Margaret Oliver (D-Druid Hills), seeks to add a special tax district to cities formed after 2005. Rep. Oliver believes that newly formed cities owe, what she refers to as, “pension legacy costs”. The notion that these legacy costs exist is false and here’s why.

- Newly formed cities continue to pay fully into the General Fund and the Fire Fund. Embedded in these funds are the costs for benefits, including pensions for the employees providing these services.

- Newly formed cities continue to pay fully into the self-sustaining funds of Sanitation and Watershed. Embedded in these funds are the costs for benefits, including pensions for the employees providing these services.

- DeKalb County lowered the millage rate for the Police Fund (a fund newly formed cities do not pay into) in the 2015 budget.

- DeKalb County did not reform the pension benefit system until December 2015 – 7 years after the formation of Dunwoody.

- DeKalb County used unrealistic actuarial assumptions that negatively impacted funding.

If DeKalb County believed there was a crisis in the pension plan, chiefly driven by the new cities no longer paying into the police fund, why would the county lower the police fund millage rate in 2015? If the county believed that the crisis was caused by newly formed cities, why did pension reform not occur until just a few months ago in December of 2015?

House Bill 711 is only directed at newly formed cities. It is punitive, based on false assumptions, and is not congruent with the facts. Make no mistake about it, it is a discriminatory tax aimed at Brookhaven and Dunwoody. It is a bailout that would allow DeKalb County to continue poor fiscal management. It creates a liability for new residents and business for a service they never received. Imagine an entirely new property tax layered onto the commercial engine of the region – the Perimeter market – and the affect that would have on business, growth, and sales tax revenue to the county, schools, and state. House Bill 711 is wrong and would have dire economic consequences for the region and state if passed.

*******

House Bill 711 is currently in the House Governmental Affairs Committee. Here is a list of emails for the members of that committee and the committee staff.

craig.foster@house.ga.gov (Policy Analyst)

michelle.spearman@house.ga.gov (Admin. Assistant)

*******

Understanding DeKalb’s Millage rate system

First, DeKalb County’s millage rate isn’t one millage rate that funds all aspects of the county. DeKalb’s total millage rate is actually the sum of various component millage rates. I often refer to these individual rates as “buckets”. Here’s a list of some of the “buckets” for which you may pay a millage rate:

- General Fund – This funds services that are provided county-wide like the court system, sheriff, libraries, etc.. It is the largest fund and every resident in DeKalb, including all cities, pays the rate for this fund.

- Fire Fund – This funds the Fire Department that is used by the unincorporated parts of the county, as well as most of the cities, included Dunwoody, Brookhaven, Chamblee, Doraville, etc.

- Police Fund – This funds the DeKalb Police Department for unincorporated DeKalb and any city that elects to use this service.

- Roads and Drainage – This funds roads and drainage services to the county and any city that elects to use this county service.

- Parks and Recreation – This funds parks and recreation services to the county and any city that elects to use this county service.

- There are also debt service rates that are apportioned county-wide and otherwise pursuant to their issuance.

- House Bill 711 proposes to add a new “bucket” that would be filled only by cities formed after 2005.

Sanitation and watershed services are self-sustaining and charge a fee-for-service for unincorporated county residents as well as residents of cities. Newly formed cities have all continued using DeKalb as their sanitation service provider. Water is only provided by the county so all cities use, and pay, for this service.

Planning and Sustainability is a self-sustaining, fee-for-service fund that provides the plan review services to residents and builders who need permits. This area also handles business licensing services. Dunwoody and Brookhaven now provide this service as a city.

Since the incorporation of Dunwoody and Brookhaven, residents of these cities have continued to pay fully into the General Fund, the Fire Fund, the appropriate debt service, and they continue to pay into the self-sustaining funds of sanitation and watershed. So, the only services that these cities no longer receive, or pay for, from the county that are funded by property tax millage rates are: (1) Police, (2) Roads and drainage, and (3) Parks and Recreation.

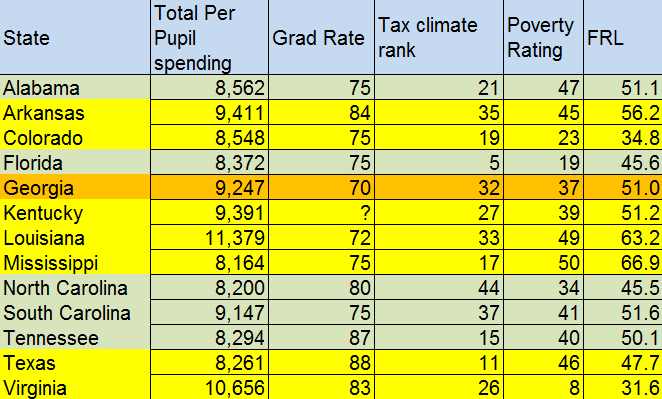

Georgia Education Per Pupil Spending, Graduation Rates, Tax Climate, Poverty Rating & Free/Reduced Lunch Percentage

In January, I posted this blog about education spending and results in Georgia.

In May, the US Census office released updated per pupil spending numbers. I have updated my regional map with these numbers, along with Georgia’s tax climate ranking, poverty ranking and the percentage of students receiving free/reduced lunch.

Georgia is still spending more per pupil and has a lower gradation rate than all of our border states. Texas, Tennessee and Mississippi all spend less per pupil, have higher graduation rates, better tax climate rankings and more poverty than Georgia. South Carolina and North Carolina both spend less, have higher graduation rates, similar poverty rankings but are rated below Georgia in tax climate. But look for both South and North Carolina to improve their tax climate rankings. North Carolina passed a major tax reform bill this year. South Carolina is working on a major overhaul.

Per Pupil Spending and Graduation Rates

Spending, rate and ranking data

What is Grover Norquist Referring To?

Hey Nancy,

Local Boards of Education are required to publish tax and expenditure data. See https://ted.cviog.uga.edu/ted/Default.do . Don’t know what Grover Norquist is referring to, but it appears [you are] campaigning on something that is already there.

What’s up with that?

Del Parker

Accounting Manager at Ga Dept of Education

![]()

Follow The Money

Follow the money. That phrase was popularized during the Watergate tumult. It is also a wise directive for all taxpayers in our state and beyond when it comes to how we spend your tax dollars on education.

So, what happens when you can’t “follow the money” because the government and the Iron Triangle Education Bureaucracy puts obstacles in your way? The Cato Institute has released a study about the transparency in spending by departments of education. It turns out Georgia earned an “F”. Click here to see their study. About Georgia, Cato points out, “Georgia is missing the most recent year of expenditures and fails to provide a table or graph that would allow citizens to easily compare changes in spending over time.” In fact, Georgia is missing the most recent 2 years. The financial data that is provided through the state DOE website is the 2010-2011 school year – a full 2 years behind our current fiscal year. (School districts have fiscal years that run from July 1 through June 30. The fiscal year is referenced by the year in which it ends.) So we are missing FY12 and FY13 on the fiscal reports.

Until we fix the financial issues that plague Georgia’s educational spending, we won’t fix education in our state. Unfortunately, Georgia’s Department of Education has not held districts accountable for how they spend your tax dollars. It appears the DOE’s only retort is to ask for more of your money. Our DOE continues to send hundreds of millions of your dollars to districts that do little to improve the educational lives of our children or even provide transparency in their expenditures. It’s all a bit cozy. Sadly, administrators have grown their take of your money over time and let smaller amounts accrue to the teachers in the classroom. Dr. Scafidi’s study, The School Staffing Surge, on how administrative staffing has grown over time in excess of student growth. In an upcoming “Coffee Talk”, we’ll cover the finances of education in Georgia and how they have hurt taxpayers, students and teachers all while benefiting the educational bureaucrats. Follow the money, indeed.

Nancy Jester says on May 13, 2014 at 2:24 pm

I hope this offers clarity:

I am advocating for adopting a system of financial integrity indicators that are rated and disclosed via a report generated by the State DOE. I would like to see us adopt a system similar to the Financial Integrity Reporting System of Texas (FIRST). This system collects data on 20 indicators of fiscal health for each district in Texas (they have over 1000). Each indicator is scored and a composite FIRST rating is then given to the district. Districts are required to hold a public meeting to discuss and disclosure their FIRST rating. Furthermore, Texas has a list of consequences for districts with poor performance records, including poor fiscal management. We have nothing like this in the state of Georgia.

Here is what the Texas Education Agency says of the FIRST:

The purpose of the financial accountability rating system (Texas Administrative Code (TAC), Title 19, § 109.1001) is to ensure that school districts and open-enrollment charter schools are held accountable for the quality of their financial management practices and achieve improved performance in the management of their financial resources. The system is designed to encourage Texas public schools to manage their financial resources better in order to provide the maximum allocation possible for direct instructional purposes. The system will also disclose the quality of local management and decision-making processes that impact the allocation of financial resources in Texas public schools.

I also advocate for on-line check registers. Most districts in Texas now have these so that taxpayers can see timely data for each financial transaction. They can find this information easily on the district’s website. There is no need to hunt for data or only have access to old information.

The Cato Institute released a report titled “Cracking the Books” in which Georgia received an F for reporting of educational expenditures. I agree that we need to improve our financial reporting and disclosure for our educational tax dollars. School districts are not even required to hold a public review of their proposed budget. (If there is a change to the millage rate they must hold meetings about that.) This year HB 886 was introduced to require school districts to hold 2 public meetings prior to passing the budget, requires the budget be placed online, and requires that a line item budget be made available upon request at no charge.

Another missing aspect in Georgia’s stewardship of the public’s money is that we do not determine the efficacy of each dollar spent. Other states are performing studies where they are “studying the intersection of academic progress and spending for efficiencies in public education.” Georgia should be doing this as well.

The Georgia DOE website does not offer an intuitive and helpful system of data that can combine relevant and timely information on the finances of each district. Georgia’s citizens should be able to access a report that not only has financial data but also the correlating achievement and staffing data. This will allow Georgia’s citizens to see the results they are getting for the dollars they are spending.

The bottom line is that HOW we spend the taxpayers’ money will drive results. We are not even measuring this. We make getting information difficult and often provide old data. We must do better.